Report

8 min read

• May 5, 2026Growing Low Carbon Solutions

- With our expertise in molecule management, we are positioned to scale a portfolio of lower-emission energy solutions through our Low Carbon Solutions (LCS) business.

- Our strategic focus on the U.S. Gulf Coast leverages the existing infrastructure and client base that make the region an industrial powerhouse for cost-effective decarbonization.

- Supportive policy is critical to drive projects in this nascent industry, and a transition to market-forming policies is needed to help fully grow LCS in the long term.

Report

8 min read

• May 5, 2026Navigate to:

Accelerating the world’s paths to net zero by building a new business with new markets

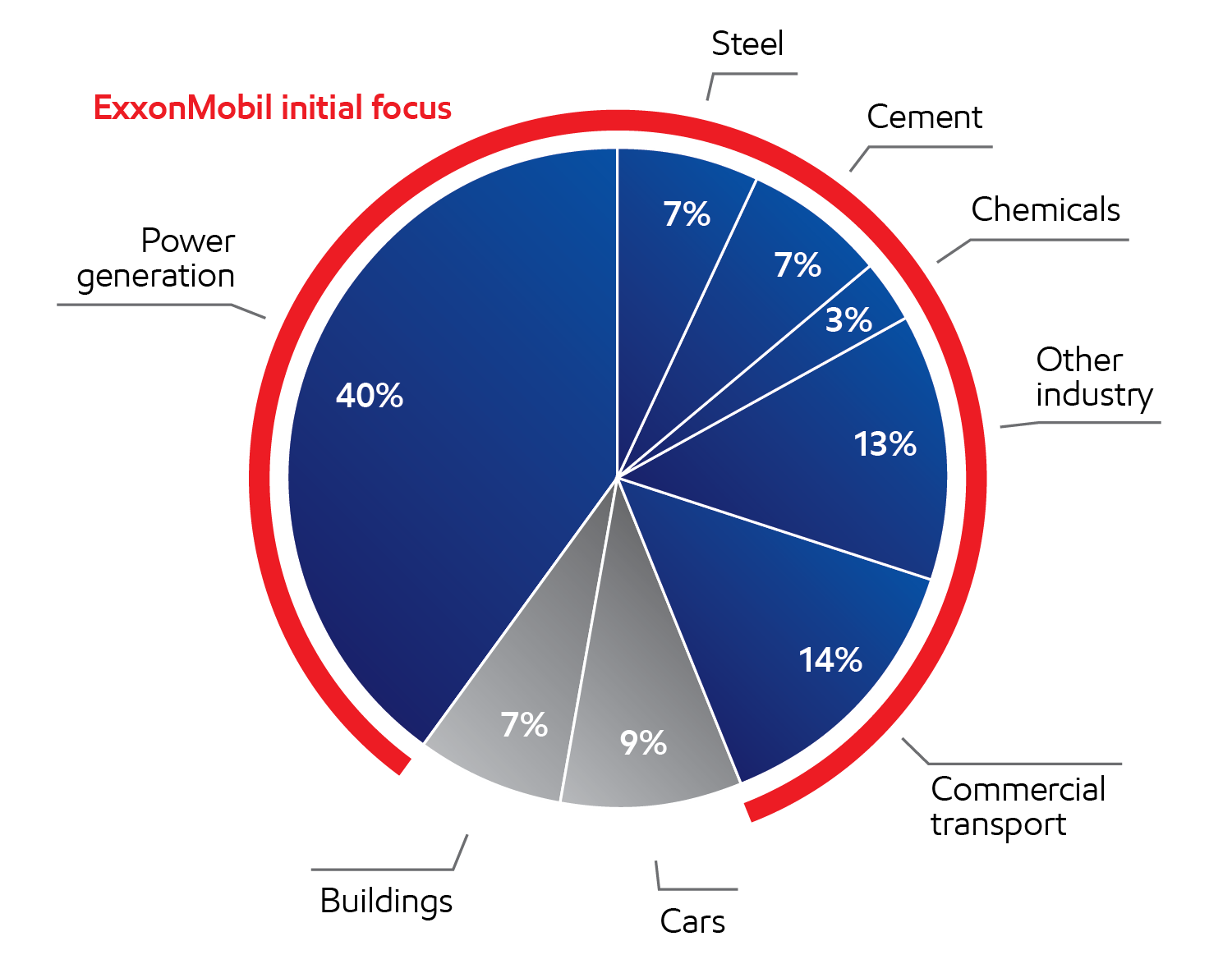

The world currently generates about 37.5 billion metric tons of CO2 emissions per year.

Industrial activity, power generation, and commercial transportation together account for about 85% of those emissions.1

This provides significant opportunities – not just for our Low Carbon Solutions business but also for other businesses in our portfolio.

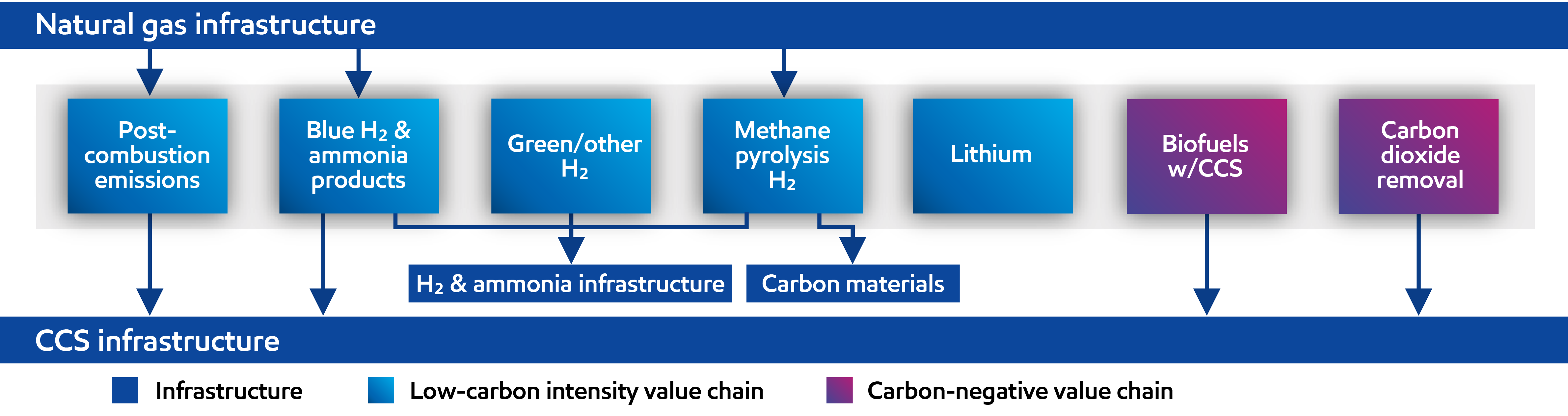

Over the past few years, we’ve established a strong foundation of opportunities in our Low Carbon Solutions business, tightly aligned with our core strengths in technology, molecular transformation, and large-scale manufacturing. They’re part of our uniquely rich slate of new business opportunities creating a long runway of profitable growth – and potential GHG emissions reductions – for decades to come.

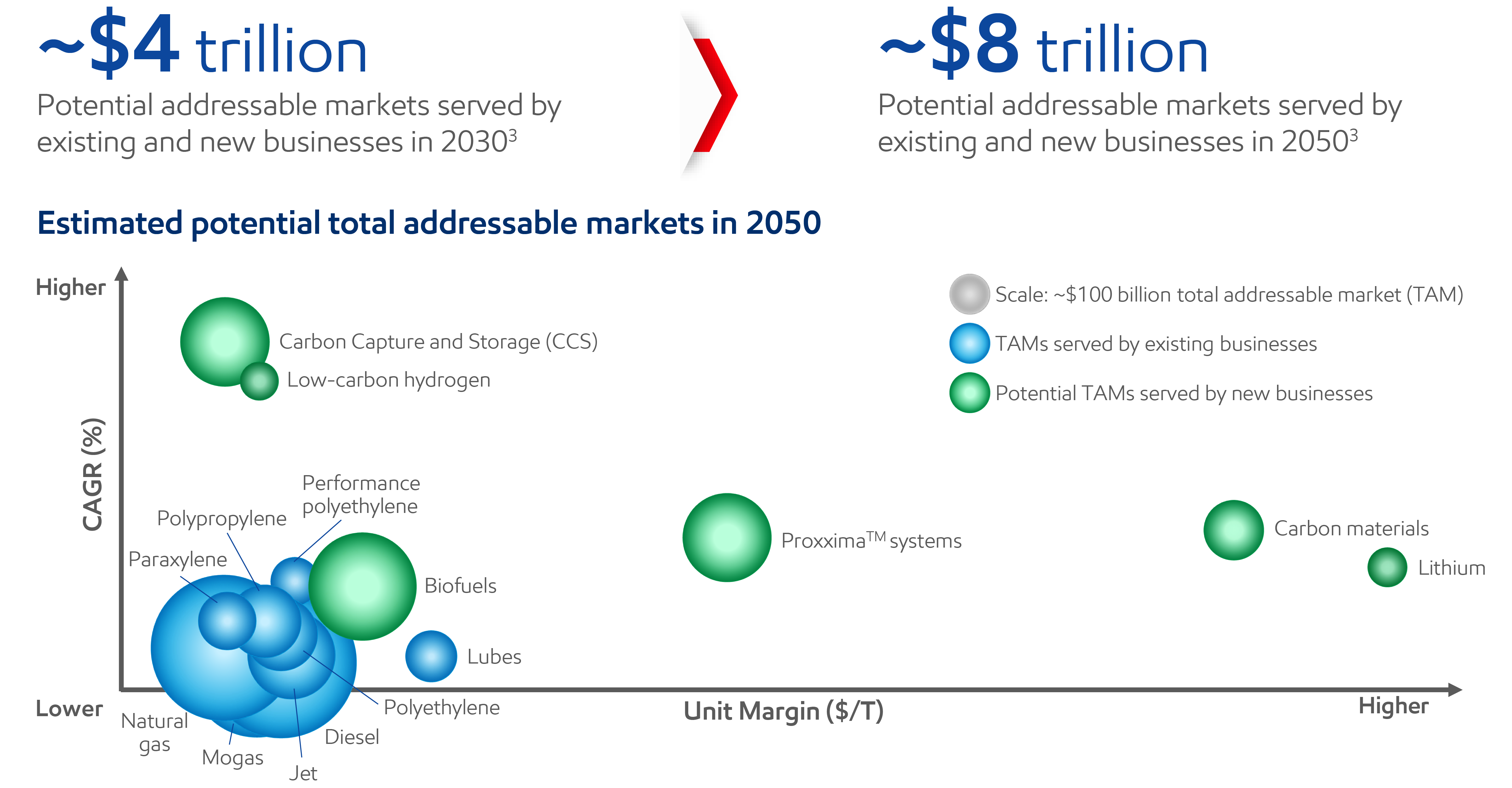

Potential addressable markets served by new and existing businesses

Our ability to manage molecules aligns with our core competencies in the low-carbon space. We have the necessary scale and infrastructure to bring these technologies to market subject to supportive policies, spurring innovation and reducing the cost of GHG emissions reduction.

The work we do includes technologies to capture, move, and store CO2; produce hydrogen from different sources; and use lower‑carbon‑intensity materials as feedstocks. All these technologies align with the competitive advantages we’ve built in our traditional businesses.

We understand our role in helping reduce emissions and the unique and important contributions we can make. Likewise, our customers, many governments, and strategic partners see how our experience, skills, and capabilities can meaningfully help reduce emissions for ourselves and others.

Investing in a lower-emission future

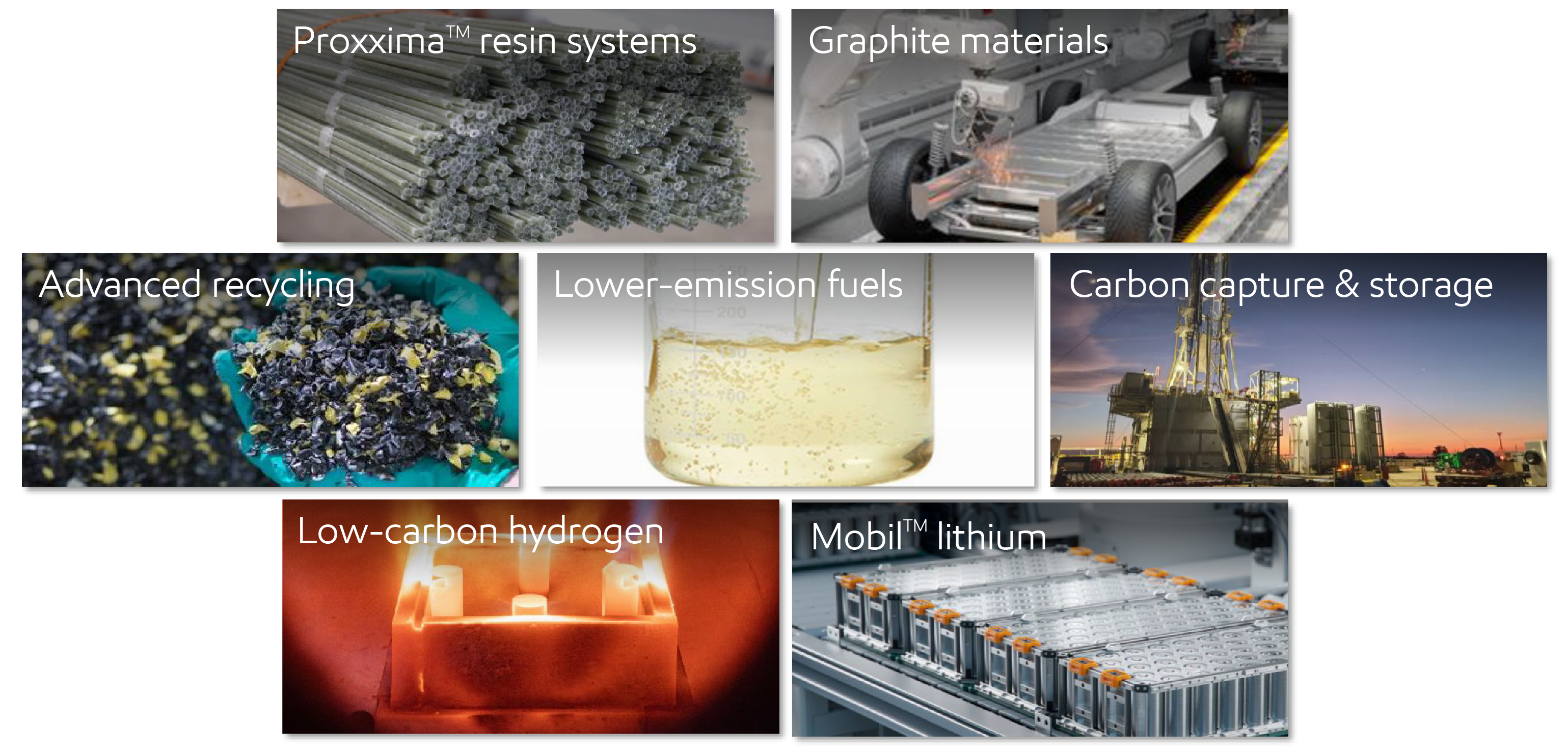

Our slate of new business opportunities is unique, leveraging our core strengths in technology, molecular transformation, and large-scale manufacturing. These opportunities exist both in our Low Carbon Solutions business and other areas of the company.

Pacing of these opportunities will continue to depend on the development of supportive policy and broader market formation, balancing risks and opportunities to help ensure strong returns and delivery of shareholder value.

By 2030, we expect these opportunities to generate more than $1 billion a year in earnings.4 As they scale, with supportive policy and market development, they have the potential to reach approximately $13 billion in earnings by 2040.5

Our intent is to pursue about $20 billion in lower-emission capital investments from 2025 through 2030.6

Meeting society’s needs requires more affordable energy and fewer emissions – at the same time. To do both, the world needs rational, constructive policy. Learn more in the Rational and constructive policy section of this report.

The role of rational and constructive policy

Because of cost, government policy is a critical part of building new low-carbon markets, especially in the near term. Supportive policies are needed to drive projects in the early stages, and we have the expertise and network to bring technology to the market.

We support legislation grounded in open markets and clear, transparent, and technology-neutral policies that avoid market distortions. By contrast, European policy continues to be more prescriptive and limits solutions for hard-to-decarbonize sectors to those that fit within certain ideologies. At this early stage, constructive policy remains critical to enable emissions reductions, advance technology, and drive scale to lower costs. Ultimately, to accelerate the world’s paths to a lower-emission future, competitive markets for emissions reduction need to develop – and rational and constructive policy is the only way that happens.

For example, we support a policy and regulatory framework for carbon capture and storage that would:

- Provide standards to ensure safe and secure CO2 storage.

- Allow for fit-for-purpose CO2 injection well design standards.

- Provide legal certainty for geologic storage ownership.

- Ensure a streamlined permitting process for carbon capture and storage facilities.

- Enable interstate CO2 pipeline expansion.

- Provide access to CO2 storage capacity owned or controlled by governments.

- Help develop carbon credits based on life cycle analysis of carbon-removal projects.

- Sustain long-term government support for research and development.

Carbon capture and storage

What it is

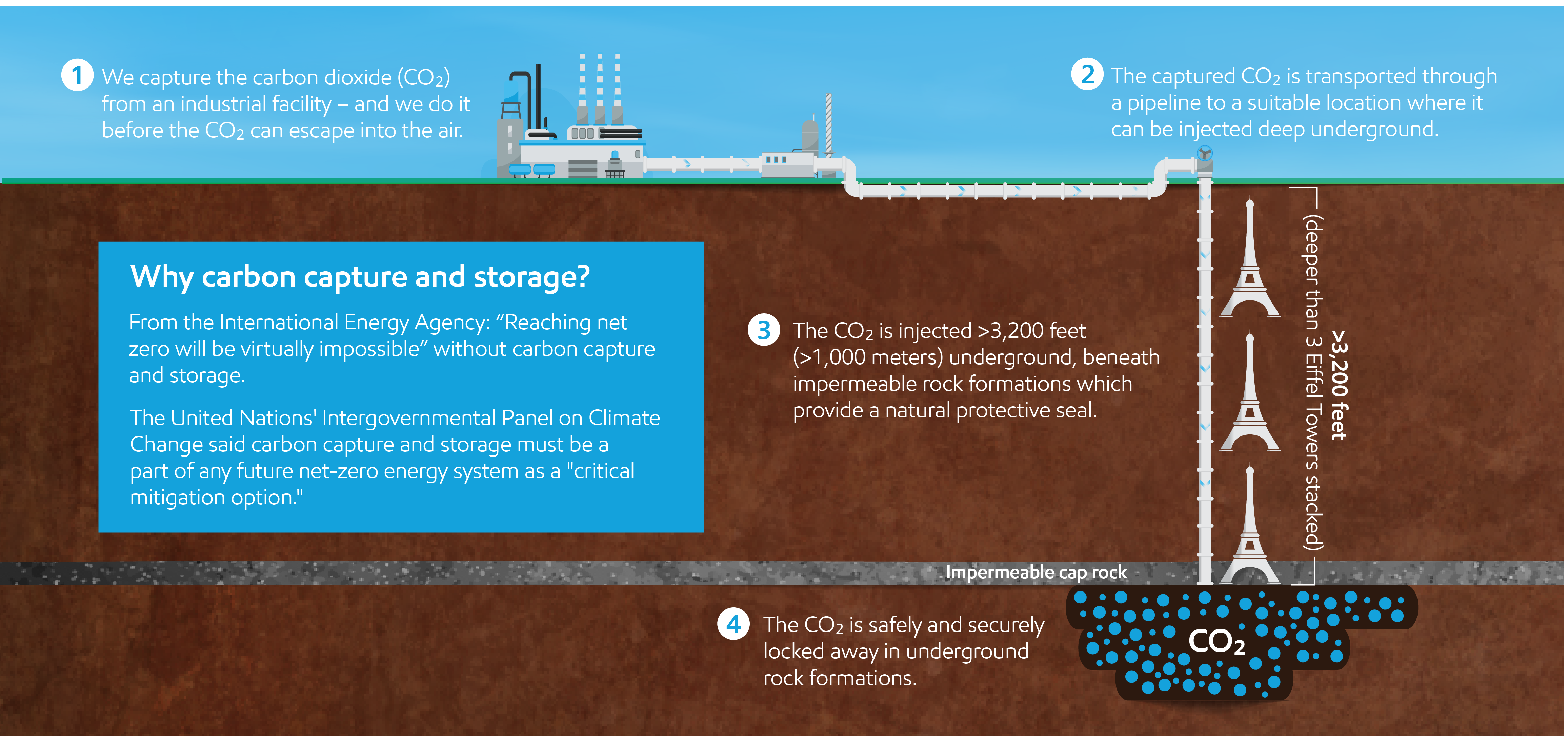

Carbon capture and storage is just what the term implies. Once CO2 is captured at factories or power plants, it is transported and injected into geologic formations thousands of feet below the earth’s surface for safe and secure storage. The CO₂ is held in place by thick, impermeable-seal rocks.

Carbon capture and storage, on its own or combined with hydrogen production, is one of the few proven technologies that could drive significant CO2 emission reductions from high-emitting and hard-to-decarbonize sectors. These include power generation, refining, steel, cement, and chemicals manufacturing. According to the Center for Climate and Energy Solutions, carbon capture and storage can capture more than 90% of CO2 emissions from power plants and industrial facilities.7

We identify opportunities with concentrated streams of CO2 near sites with safe and secure storage space, and where we can use existing infrastructure to gain scale to offer cost-effective solutions to customers.

What we’re doing

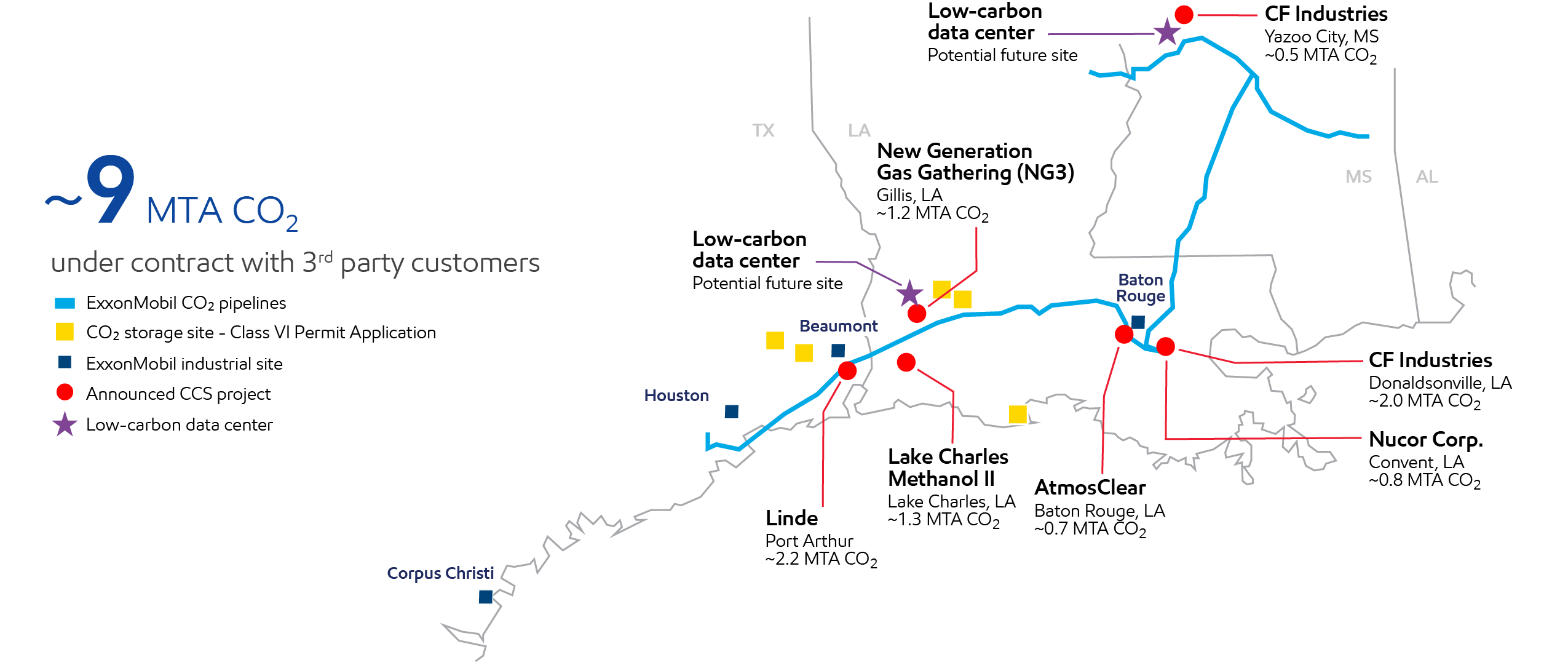

We have the world's first large-scale end-to-end carbon capture and storage system.8 With more than 1,300 miles of owned and operated pipeline and more than 30 years of experience in carbon capture, we are continuing to develop and expand our capacity for storing CO2 on a long-term basis.

Our initial CCS activity is focused on the U.S. Gulf Coast. This region has the critical drivers needed to provide a lower-cost decarbonization solution for industrial applications: a high concentration of large emitters, geologic storage space, and existing transportation infrastructure. These drivers, strengthened by policy like the IRA, are helping us build a carbon capture and storage network that can help our industrial customers significantly reduce their emissions.

The U.S. Gulf Coast has a large concentration of CO2 emissions – with one third of all U.S. industrial emissions coming from this region.9

This makes it a great strategic fit as about 70% of our CCS pipelines are located in the Gulf Coast states of Louisiana, Texas, and Mississippi. This transport and storage network can support multiple low-carbon businesses – including carbon capture and storage, hydrogen, ammonia, and biofuels. And it has been designed to reliably connect a wide range of CO2 emitters to storage locations.

We continue to add suitable acreage onshore and offshore to expand our storage capacity. Our advantaged infrastructure and deep experience in molecule management put us in the lead to deploy CCS at scale. Building on our successful collaborations with host governments, we are also negotiating to gain access to nationally owned acreage that holds potential for CO2 storage. We also continue to work with local jurisdictions on the appropriate permitting to store CO2, which will be essential to the success of these projects.

Further, we secured from the Texas General Land Office the largest offshore CO2 lease in the United States, at just over 271,000 acres.

Real projects, real progress

Another vital element of establishing a successful business is building a customer base, and we’re making great progress.

- CF Industries Is a leading global manufacturer of hydrogen and nitrogen products. They signed commercial agreements with us to capture and permanently store up to ~2.5 million metric tons of CO2 emissions annually from manufacturing complexes in Louisiana and Mississippi. In July 2025, we began transporting and storing CO2 from their Donaldsonville Complex, enabling the production of low-carbon ammonia.

- Linde is one of the world's leading industrial gases and engineering companies. They entered into a long-term commercial agreement with us in which we plan to transport and permanently store up to ~2.2 million metric tons of CO2 annually from their clean hydrogen production facility in Beaumont, Texas.

- Nucor Corp. is North America’s largest steel and steel products producer. They entered into a long-term commercial agreement with us where we will capture, transport, and store up to ~800,000 metric tons of CO2 annually from their manufacturing site in Convent, Louisiana.

- New Generation Gas Gathering (NG3) is the first natural gas customer to use our CCS infrastructure. ExxonMobil is now transporting and storing captured CO2 from the NG3 project in Louisiana, with up to 1.2 million metric tons of CO2 per year under contract.

- Lake Charles Methanol II has contracted with us to transport and store up to ~1.3 million metric tons of CO2 annually from their project in Louisiana, where they plan to use advanced natural gas reforming and permanent geologic storage solutions to produce low-carbon hydrogen and methanol.

- AtmosClear has contracted with us to transport and store ~700,000 metric tons of CO2 annually from their greenfield bio-power plant west of Baton Rouge, Louisiana, with the potential for additional volumes. Separately, AtmosClear has announced a 15-year CO2 removal credit offtake agreement with Microsoft.10

This adds up to about 9 million tons per year of CO2 under contract – equal to replacing about 4 million cars with electric vehicles, which is roughly 3 times the total number of EVs sold in the U.S. in 2025.

Advantaged U.S. Gulf Coast position11

What’s next

- Building our customer base: We continue to work with others in the industry to spur advances in technology to lower cost and further build our customer base. We see potential to reduce CO2 emissions across the U.S. Gulf Coast by more than 100 million metric tons per year.12

- Policy advocacy: Land access is critical to accelerating carbon capture project deployment – onshore and offshore. We continue to advocate for streamlined permitting and regulation for long-term CO2 storage.

- Studying storage: We are working with leading universities and other research organizations to advance knowledge in monitoring requirements and modeling of geologic storage. This work includes seal characterization for containment assessment,13 as well as optimal long-term monitoring of stored CO2.

- Low-carbon data centers (LCDC): Globally, energy demand for data centers is projected to more than double over the next five years, driven by the increasing demand for artificial intelligence – and almost half of this growth will be in the U.S.14 We’re advancing our first LCDC project, with potential sites in Louisiana and Mississippi. We already have firm turbine commitments, proven capture capability, and active negotiations with hyperscaler customers.

What respected third parties are saying about carbon capture and storage

Both the International Energy Agency (IEA) and the United Nations Intergovernmental Panel on Climate Change (IPCC) see carbon capture and storage as key to reaching global emissions ambitions. The IPCC states, “In the majority of the scenarios reaching low GHG targets, a considerable amount of CCS is applied."15

The IEA concludes that more than 6 billion metric tons per year of CO2 will need to be captured and stored by 2050 to reach a net-zero future.16 By comparison, the world’s current capture capacity is far below that at about 50 million metric tons of CO2 per year.17 The agency has also said “reaching net zero will be virtually impossible” without carbon capture and storage.18

It’s worth noting that there is a very small but vocal fringe who oppose CCS for their own reasons, often repeating inaccurate claims about efficacy or safety. These objections fly in the face of established science supported by both U.S. political parties, prominent eNGOs, the United Nations, and half a century of evidence since the technology was first deployed in the 1970s.

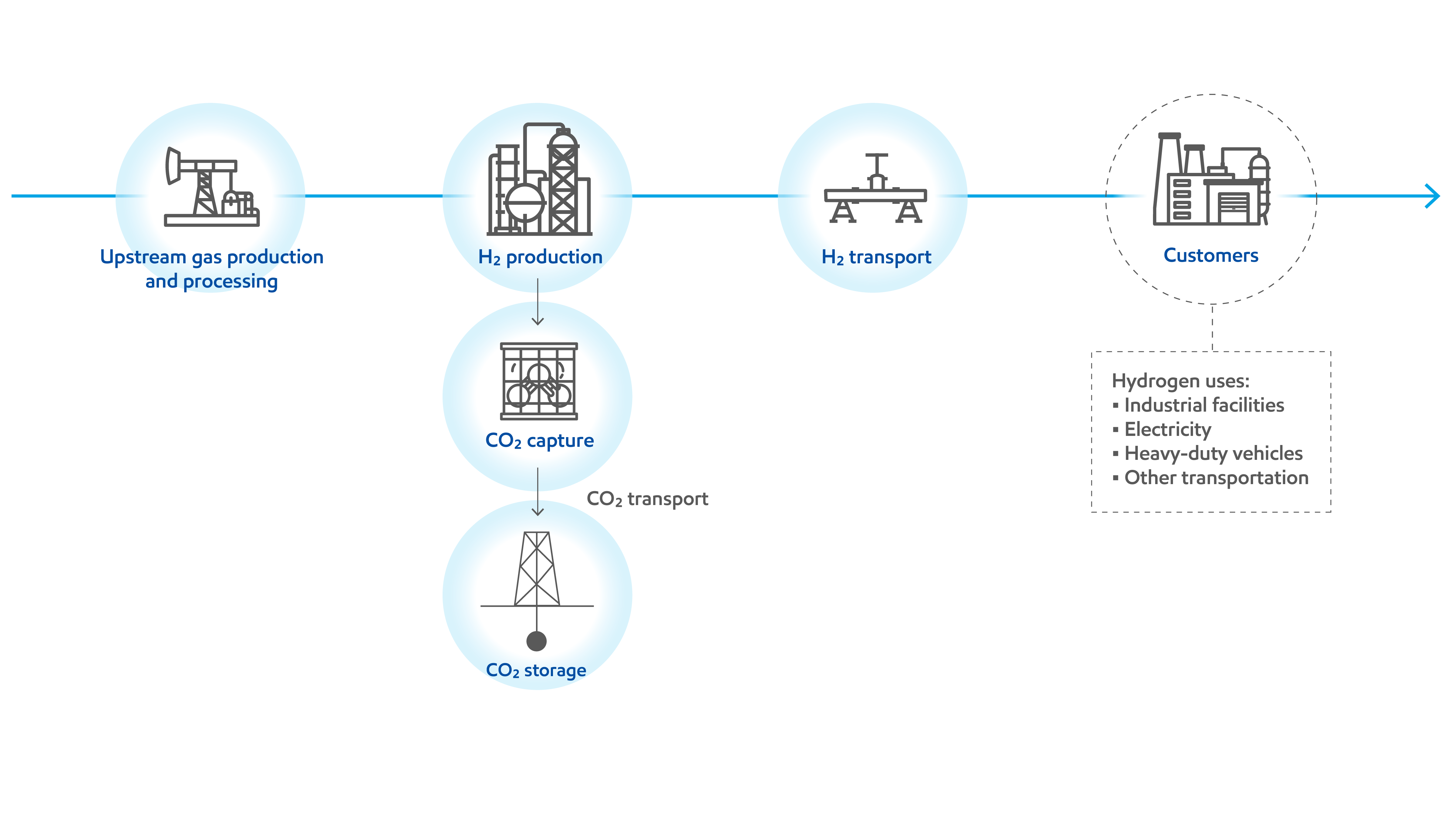

Hydrogen

What it is

When used for energy, hydrogen does not emit carbon, and it can generate the high temperatures needed to produce steel, cement, and refining and chemical products without carbon dioxide emissions. This means it could serve as an affordable and reliable source of energy for hard-to-decarbonize industrial processes.

What we’re doing

Just as we have a long history with carbon capture and storage, we have deep and broad experience with hydrogen. We use hydrogen in just about every one of our refining and chemical plants.

In 2025, we announced a pause in the development of our efforts in Baytown, Texas, to produce virtually carbon-free hydrogen (with ~98% of CO2 captured and stored). We have consistently said that lower-emissions investments like this depend on supportive policy and market developments. Despite our best efforts, neither policy nor the market was sufficient to warrant our continued investment, and we continue to engage with customers and policymakers in an effort to help create the necessary conditions to resume our work.

And we’re continuing to advance new uses and ways to produce this important, lower-carbon-emission energy source:

- Hydrogen burners: Temperatures inside the furnaces that “crack” hydrocarbon molecules into olefins exceed 2,000°F – and it’s an energy-intensive process. Fuel-switching to hydrogen has the potential to significantly reduce GHG emissions-intensity, because hydrogen emits no CO2 when combusted.

At our plant in Baytown, we’ve designed and installed pyrolysis burners that can operate on hydrogen fuel. Our testing of a 98% hydrogen fuel mix successfully produced ethylene and other olefins – with a 90% reduction in direct CO2 emissions.19

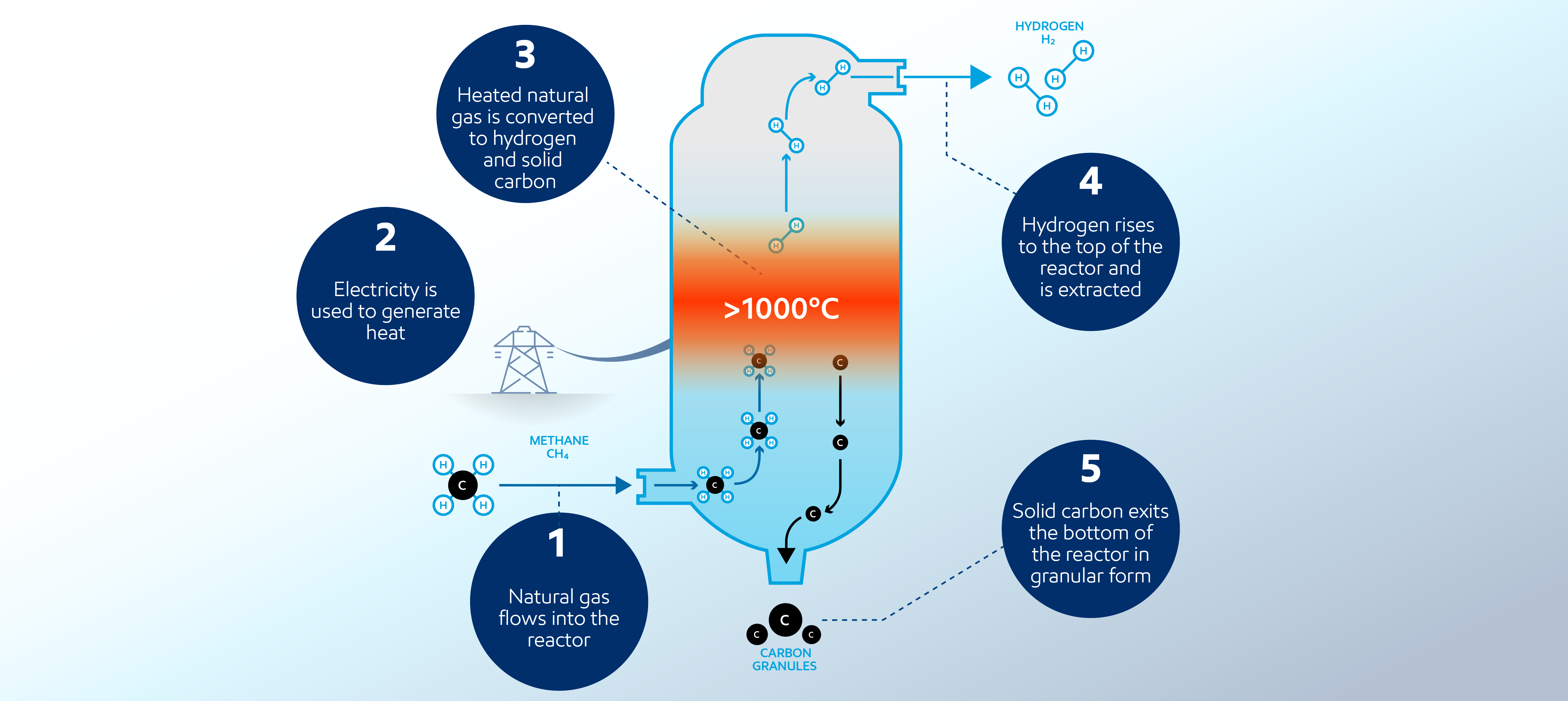

- Methane pyrolysis: ExxonMobil is advancing a novel methane pyrolysis technology, in a strategic collaboration with BASF, that can produce affordable, low carbon-emission hydrogen and high-purity solid carbon for a wide range of industrial uses.

The process uses electricity to convert natural gas or other gases, like bio-methane, into valuable molecules. It needs approximately five times less electricity than water electrolysis, uses no water, and emits zero process-related CO2. This technology leverages existing natural gas infrastructure, so it can be deployed even in areas without access to CCS. A demonstration plant capable of producing up to 2,000 tons of low-emission hydrogen and 6,000 tons of solid carbon product annually is planned in Baytown to validate the technology at scale.

Methane pyrolysis converts natural gas into hydrogen and solid carbon

What’s next

- Policy advocacy: We advocate for durable, predictable, and market-driven policy support, taking a thoughtful and pragmatic approach that we believe is a win/win for our business and for society.

- Research and development: We are working with universities to expand understanding of the end-to-end carbon emissions from different technologies, including hydrogen. For example, the life-cycle tool we helped to develop as part of the Massachusetts Institute of Technology (MIT) Energy Initiative is being used by policymakers and others as they consider policies to reduce global GHG emissions at the lowest cost to society.20

What respected third parties are saying about hydrogen

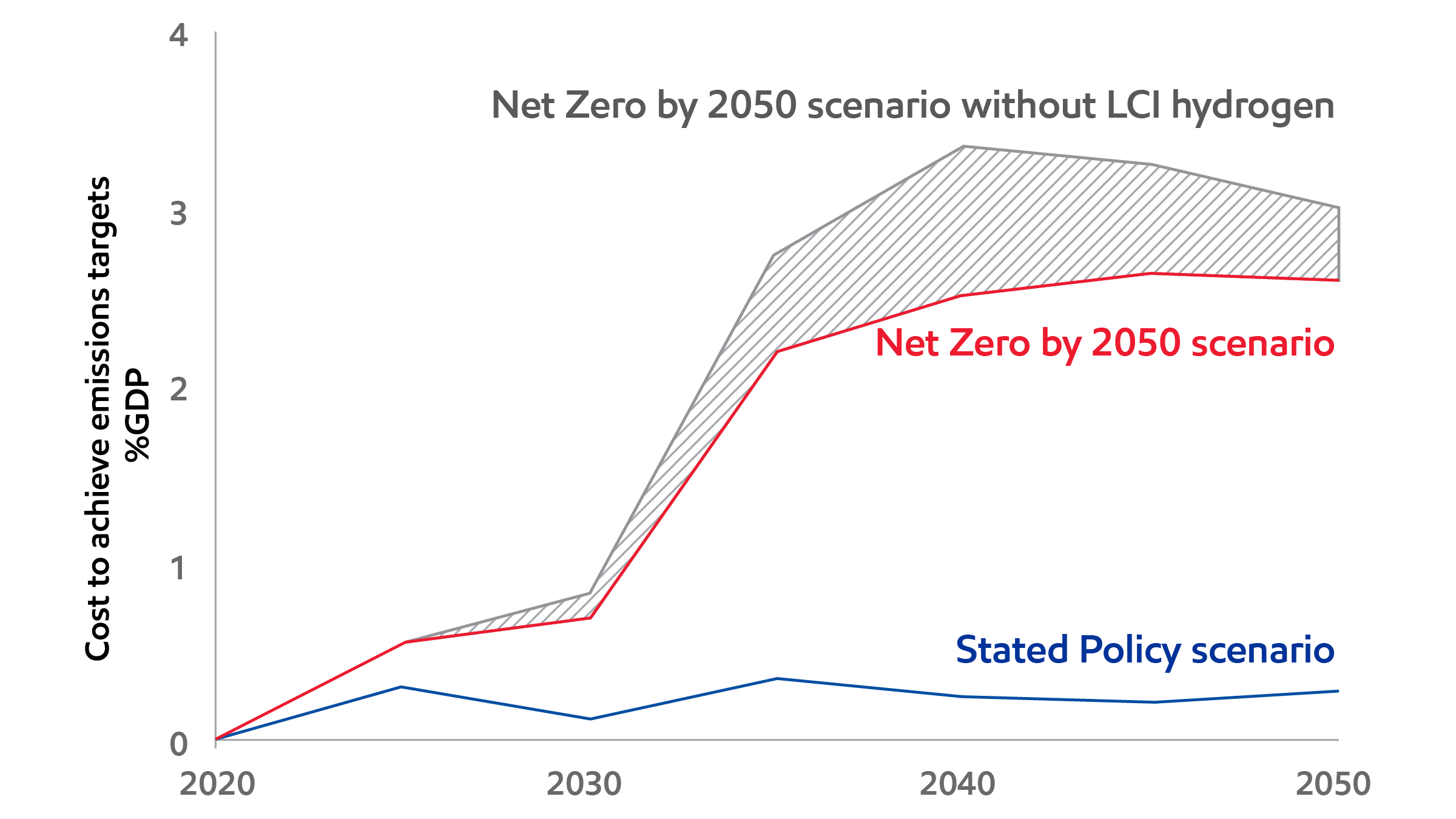

In 2024, the National Petroleum Council (NPC) published “Harnessing Hydrogen: A key element for the U.S. Energy Future.” The study details deployment of low-carbon-intensity hydrogen at scale in the United States.

The NPC assembled a diverse team of more than 300 experts from over 100 organizations, 70% of which come from outside of the oil and natural gas industry. This study applied scenario-based modeling, partnering with the MIT Energy Initiative.

The key finding? Deploying lower-carbon hydrogen at scale in hard-to-abate sectors in the United States can lower the cost of reducing carbon emissions. In fact, under MIT’s Net Zero by 2050 scenario, achieving net zero would cost approximately 30% more without hydrogen.21

Low-carbon-intensity (LCI) hydrogen can play a key role in achieving emissions reduction at a lower cost to society22

Lower-emission fuels

What they are

These fuels generate fewer GHG emissions over their life-cycles than the traditional fuels they replace. They include biofuels made from renewable sources like plants and waste, biomass and synthetics made from hydrogen, and captured CO2 to form methanol. Lower-emission fuels have the high energy density required to move heavy trucks, airplanes, trains, and ships. Renewable diesel may reduce life-cycle carbon emissions by up to 80% compared to conventional diesel.23 Demand for these fuels is expected to grow rapidly. Our Global Outlook projects biofuel demand in the global transportation sector to increase through 2050.24

Our Product Solutions business is working to grow lower-emission fuels by applying our strengths in technology, scale, integration, and infrastructure. At the same time, our Low Carbon Solutions business is working to develop lower-emission fuels, underpinned by our other low-carbon businesses.

We’re exploring the combination of biomass-based fuel production with carbon capture and storage. This opportunity could open the door to very low- or negative-carbon intensity fuel production. Lower-emission fuels can utilize existing distribution infrastructure, lowering the cost of deployment.

We’re also looking at how we can efficiently transform natural gas into methanol-based fuels. And, we already have the capability to convert methanol to multiple end-use fuels, such as marine and jet fuel. This ability could enable a range of lower-emission fuels.

What we’re doing

- Canada: Our affiliate Imperial Oil’s Strathcona refinery is now producing renewable diesel. At full capacity, it is expected to be the largest renewable diesel facility in Canada – capable of producing up to 20,000 barrels a day.

- Renewable diesel blends: With lower life-cycle GHG emissions than conventional diesel, we’re selling fuel blends with up to 100% renewable diesel in a dozen countries around the world. These fuels are made with hydrotreated vegetable oil (HVO) refined from waste oils, such as used cooking oil, and they work with most modern diesel engines.

- Co-processing: Critically needed to expand the production of biofuels, co-processing is the ability to process biofeed and conventional feedstock together. Where policy allows, we continue to conduct co-processing trials in our facilities to produce lower-emission fuels. In 2025, we started up co-processing lines in Edmonton, Canada, and Antwerp, Belgium, and are providing product to those markets.

What’s next

- Maritime goals: We support the International Maritime Organization’s GHG emission-reduction goals, and the IMO recognizes the use of LNG and bio-LNG as alternative marine fuels. We are working to help our customers determine the best ways to lower their emissions. For example, we have supplied ExxonMobil bio-marine fuel oil blends in Singapore and Amsterdam-Rotterdam-Antwerp bunkering hubs, and in 2025 we announced our entry into the LNG and bio-LNG bunkering market.

- Testing with Toyota: Working with Toyota, we're continuing to explore ways to reduce life-cycle GHG emissions from the fuels used in cars today. So far the research fuel blends we’ve road tested have demonstrated that they can be compatible with today’s vehicles and have the potential to use existing infrastructure.

- New jet fuel technology: We have developed technology to produce jet fuel using renewable methanol, which can be derived from processes using biofeeds (e.g., wood waste) or low-carbon hydrogen.25 We continue to conduct R&D on other ways to produce renewable jet fuel from various biofeeds, and we're collaborating with third parties to further lower the cost of production.

Lithium

What it is

Lithium is a key component of battery technology. Batteries account for over 80% of global lithium use.26

Electric vehicles rely on lithium for their rechargeable batteries. EVs can play a key role in reducing emissions in transportation, and lithium demand is projected to increase fivefold by 2040.27 Many AI data centers count on battery energy storage systems for uninterrupted power, which is important for reliability and national security.

Most raw lithium ore is produced from hard rock mining and shipped over vast distances. Lithium prices have oscillated widely over the last couple of years as supply and demand continue to evolve, but the long-term demand outlook is encouraging – driven by EVs and energy storage.

What we’re doing

In 2023, we announced plans to produce lithium carbonate for use in EV battery manufacturing by employing direct lithium extraction (DLE) technology in our leading acreage position in the Smackover region in Arkansas.

By applying DLE technology to separate the lithium from deep brine reservoirs, we’re working to produce this critical mineral with as low as 2/3 less carbon intensity than hard rock mining.28 We believe our existing skills in subsurface exploration, drilling, refining, and chemicals will allow us to bring meaningful scale to this technology and provide auto battery manufacturers with a more reliable, lower-carbon lithium supply option.

We’ve completed our appraisal well drilling and seismic program, which has confirmed that we have an attractive resource. And we have successfully produced battery-grade lithium carbonate at our Texas pilot facility from brine extracted from southern Arkansas.

What’s next

We aim to be a leading North American supplier of lithium carbonate by the first half of the 2030s. Our domestically produced lithium will strengthen supply security for companies investing in EV and battery manufacturing facilities in North America.

We’re also sponsoring research at Southern Arkansas University to advance DLE technology. By providing funding, lab equipment and ongoing technical expertise, we’re supporting development that strengthens American innovation, builds local research capacity, and helps prepare talent for the emerging lithium industry.

Other solutions

Carbon capture and storage, hydrogen, lower-emission fuels, and lithium are only some of the emission-reduction technologies in the world – and in our portfolio. We are always looking for opportunities that fit our strengths, capabilities, and businesses.

For example, many of our natural gas and LNG customers have significant post-combustion emissions that they’d like to reduce. We offer a “one-stop shop” for CO2 capture, transportation, and storage that will help these customers reduce their emissions.

We also see a growing opportunity in the market for carbon materials like synthetic graphite. We’re expanding into the advanced synthetic graphite business with our acquisition of Superior Graphite’s U.S. assets. Our next-gen battery anode graphite is engineered to deliver 30% faster charging, up to 30% higher usable battery capacity, and up to 4x longer life than traditional graphite materials. And we’re establishing and scaling up a differentiated graphitization process – with higher throughput, up to 50% greater energy efficiency, and much shorter processing time than industry alternatives.29

We’re building on our technology, scale, project execution, and integration advantages to establish an attractive new business. We believe this new business complements our traditional businesses and will underpin the company’s growth and returns for decades to come.

Publications

Explore more

Governance and risk management

Report

•

8 min read

• May 5, 2026

Research and development

Report

•

6 min read

• May 5, 2026

Positioned for growth in a lower-emission future

Report

•

8 min read

• May 5, 2026

Driving reductions in methane emissions

Report

•

6 min read

• May 5, 2026

Rational and constructive policy

Report

•

8 min read

• May 5, 2026FOOTNOTES:

- ExxonMobil 2025 Global Outlook (Aug. 28, 2025)

- Ibid.

- Total Addressable Markets derived from our 2025 Global Outlook, other internal assessments, and third-party projections. Does not necessarily reflect our internal plans or assumptions. See page 44 of ExxonMobil 2025 Corporate Plan Update for the sources, prices, and margins references used. Source: ExxonMobil 2025 Corporate Plan Update (Dec. 9, 2025)

- New businesses earnings potential is based on internal assessment of ExxonMobil’s ability to capture Total Addressable Market potential. Roughly $13 billion of earnings potential by 2040 is subject to additional investment by ExxonMobil. Source: ExxonMobil 2025 Corporate Plan Update (Dec. 9, 2025)

- Ibid.

- Lower emissions investments include cash capex attributable to carbon capture and storage, hydrogen, lithium, biofuels, Proxxima™ systems, carbon materials, and activities to lower ExxonMobil’s emissions and/or third party emissions. Source: ExxonMobil 2025 Corporate Plan Update (Dec. 9, 2025)

- Center for Climate and Energy Solutions, https://www.c2es.org/content/carbon-capture/

- “End-to-end CCS system” entails integration of CO2 capture, transportation, and storage. Based on contracts starting in 2025, subject to additional investment by ExxonMobil, and receipt of government permitting for carbon capture and storage projects. Source: ExxonMobil 2025 Corporate Plan Update (Dec. 9, 2025)

- United States Environmental Protection Agency, GHGRP Emissions by Location (2023): https://www.epa.gov/ghgreporting/ghgrp-emissions-location.

- AtmosClear Selects ExxonMobil for CO2 Transportation and Storage https://www.prnewswire.com/news-releases/atmosclear-selects-exxonmobil-for-co-transportation-and-storage-302562371.html

- Information shown is approximate (e.g., storage / pipeline location) and has potential to change as projects are developed and implemented. CO2 storage includes Class VI Permit Application and GLO Storage Site Access. Subject to additional investment by ExxonMobil and implementation of supportive government policy, including government permitting for carbon capture and storage projects. Source: ExxonMobil 2025 Corporate Plan Update (Dec. 9, 2025)

- Market potential for emission reduction opportunity based on ExxonMobil analysis of CO2 pipeline routes, current and potential capacity, potential emitters in the U.S. Gulf Coast market, and potential infrastructure upgrades. Subject to additional investment by ExxonMobil, customer commitments, supportive policy, and permitting for carbon capture and storage projects.

- D. Tapriyal, F. Haeri, D. Crandall, W. Horn, L. Lun, A. Lee, A. Goodman, Caprock Remains Water Wet Under Geologic CO2 Storage Conditions, Geophysical Research Letters 51 (2024)

- IEA (2025), Energy and AI, IEA, Paris https://www.iea.org/reports/energy-and-ai, Licence: CC BY 4.0

- IPCC AR6 Report, Chapter 3: Mitigation pathways compatible with long-term goals (page 332): https://www.ipcc.ch/report/ar6/wg3/downloads/report/IPCC_AR6_WGIII_Chapter03.pdf

- IEA (2025), World Energy Outlook 2025, IEA, Paris https://www.iea.org/reports/world-energy-outlook-2025, Licence: CC BY 4.0 (report); CC BY NC SA 4.0 (Annex A)

- IEA (2025), CCUS Projects Explorer, IEA, Paris https://www.iea.org/data-and-statistics/data-tools/ccus-projects-explorer, License: CC BY 4.0 (report); CC BY NC SA 4.0 (Annex A)

- IEA (2020), CCUS in Clean Energy Transitions, IEA, Paris https://www.iea.org/reports/ccus-in-clean-energy-transitions, License: CC BY 4.0

- ExxonMobil calculation based on fuel composition during testing relative to the baseline average fuel composition of the furnace.

- E. Gencer, S. Torkamani, I. Miller, T. Wu, F. O’Sullivan, Sustainable energy system analysis modeling environment: analyzing life-cycle emissions of the energy transition, Applied Energy 277 (2020) 115550

- The modeling for this study estimates that reaching net zero would cost about 3% GDP. However, if LCI hydrogen is not deployed, the cost of achieving net zero could increase the cost by 0.5-1% of GDP. Assuming a GDP of $38 trillion in 2050, a 3% cost to society equates to $1.1 trillion. The impact of not deploying LCI hydrogen to achieve emission targets changes by year, ranging $160 – 260 billion between 2035 and 2050: https://harnessinghydrogen.npc.org/

- Ibid.

- Based on ExxonMobil analysis using Argonne National Labs’ GREET2023 model and published fuel carbon intensity from California LCFS regulations. Argonne National Laboratory GREET model: https://greet.anl.gov/, California Air Resources Board Low Carbon Fuel Standard Regulation: https://ww2.arb.ca.gov/our-work/programs/low-carbon-fuel-standard/lcfs-regulation

- ExxonMobil 2025 Global Outlook (Aug. 28, 2025)

- ExxonMobil Press Release (June 2023): https://www.exxonmobil.com/en/aviation/knowledge-library/resources/mtj-a-new-route-to-saf

- U.S. Geological Survey, 2025, Mineral commodity summaries 2025 (ver. 1.2, March 2025): U.S. Geological Survey, 212 p., https://doi.org/10.3133/mcs2025

- IEA (2025), Global Critical Minerals Outlook 2025, IEA, Paris https://www.iea.org/reports/global-critical-minerals-outlook-2025, Licence: CC BY 4.0

- Expected smaller footprint of lithium mining and expected lower carbon and water impacts: EM analysis of external sources and third-party life-cycle analyses. a) Vulcan Energy, 2022 https://v-er.eu/app/uploads/2023/11/LCA.pdf, Minviro publication. Grant, A., Deak, D., & Pell, R. (2020). b) The CO2 Impact of the 2020s Battery Quality Lithium Hydroxide Supply Chain-Jade Cove Partners. https://www.jadecove.com/research/liohco2impact Kelly, J. C., Wang, M., Dai, Q., & Winjobi, O. (2021). c) Energy, greenhouse gas, and water life cycle analysis of lithium carbonate and lithium hydroxide monohydrate from brine and ore resources and their use in lithium ion battery cathodes and lithium ion batteries. Resources, Conservation and Recycling, 174, 105762.

- McKinsey analysis of alternative graphitization processes for battery anode materials.

FORWARD-LOOKING STATEMENT WARNING

CAUTIONARY STATEMENT RELEVANT TO FORWARD LOOKING INFORMATION FOR THE PURPOSE OF THE “SAFE HARBOR” PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 AND OTHER IMPORTANT LEGAL DISCLAIMERS

Images or statements of future ambitions, aims, aspirations, plans, goals, events, projects, projections, opportunities, expectations, performance, potential addressable markets or conditions in the publications, including plans to reduce, abate, avoid or enable avoidance of emissions or reduce emissions intensity, sensitivity analyses, estimates, the development of future technologies, business plans, and sustainability efforts are dependent on future market factors, such as customer demand, continued technological progress, stable policy support and timely rule-making or continuation of government incentives and funding, and represent forward-looking statements. Similarly, emission-reduction roadmaps to drive toward net zero and similar roadmaps for emerging technologies and markets, and water management roadmaps to reduce freshwater intake and/or manage disposal, are forward-looking statements. These statements are not guarantees of future corporate, market or industry performance or outcomes for ExxonMobil or society and are subject to numerous risks and uncertainties, many of which are beyond our control or are even unknown.

Actual future results, including the achievement of ambitions to reach Scope 1 and 2 net zero from operated assets by 2050, to reach Scope 1 and 2 net zero in integrated Upstream Permian Basin unconventional operated assets by 2035, to eliminate routine flaring in-line with World Bank Zero Routine Flaring, to reach near zero methane emissions from operated assets and other methane initiatives to meet ExxonMobil’s greenhouse gas emission reduction plans and goals, divestment and start-up plans, and associated project plans as well as technology advances, including in the timing and outcome of projects to capture, transport and store CO2, produce hydrogen and ammonia, produce lower-emission fuels, produce ProxximaTM systems, produce carbon materials, produce lithium, and use plastic waste as feedstock for advanced recycling; future debt levels and credit ratings; business and project plans, timing, costs, capacities and profitability; resource recoveries and production rates; planned Denbury and Pioneer integrated benefits; detection, measurement and quantification of emissions including obtaining or reporting of that data or updates to previous estimates and progress in sustainability focus areas could vary depending on a number of factors. These include, global or regional changes or imbalances in the supply and demand for oil, gas, petrochemicals, and feedstocks and other market factors; economic conditions and seasonal fluctuations that impact prices, differentials, and volume/mix for our products; new market products and services; future cash flows; our ability to execute operational objectives on a timely and successful basis; the ability to realize efficiencies within and across our business lines; developments or changes in local, national, or international treaties, laws, regulations, taxes, trade sanctions, trade tariffs, or policies affecting our business, such as government policies supporting lower-carbon and new market investment opportunities, or policies limiting the attractiveness of investments such the punitive European taxes on the oil and gas sector and unequal support for different technological methods of emissions reduction or evolving, ambiguous, and unharmonized voluntary and mandatory standards and extraterritorial laws and regulations imposed by various jurisdictions related to sustainability and greenhouse gas reporting and evolving measurement standards for these topics; timely granting of governmental permits, licenses, and certifications; uncertain impacts of deregulation on the legal and regulatory environment; trade patterns and the development and enforcement of local, national and regional mandates; unforeseen technical or operational difficulties; the outcome of research efforts and future technology developments, including the ability to scale projects and technologies such as electrification of operations, advanced recycling, carbon capture and storage, hydrogen and ammonia production, ProxximaTM systems, carbon materials or direct lithium extraction on a commercially competitive basis; the development and competitiveness of alternative energy and emission reduction technologies; unforeseen technical or operating difficulties, including the need for unplanned maintenance; availability of feedstocks for lower-emission fuels, hydrogen, or advanced recycling; changes in the relative energy mix across activities and geographies; the actions of co-venturers or competitors; changes in regional and global economic growth rates and consumer preferences including willingness and ability to pay for reduced emissions products; actions taken by governments and consumers resulting from a pandemic; changes in population growth, economic development or migration patterns; timely completion of construction projects; war, civil unrest, attacks against the Company or industry, and other political or security disturbances, including disruption of land or sea transportation routes; decoupling of economies, realignment of global trade and supply chain networks, and disruptions in military alliances; and other factors discussed here and in Item 1A. Risk Factors of our Annual Report on Form 10-K and under the heading “Factors affecting future results” available under the “Earnings” tab through the “Investors” page of our website at www.exxonmobil.com. The Advancing Climate Solutions Report includes 2025 greenhouse gas emissions performance data as of March 13, 2026, and Scope 3 Category 11 estimates for full year 2025 as of March 13, 2026. The greenhouse gas intensity and greenhouse gas emission estimates include Scope 2 market-based emissions. The Sustainability Report, the Advancing Climate Solutions Report, and combined Executive Summary were issued on May 5, 2026. The content and data referenced in these publications focus primarily on our operations from Jan. 1, 2025 – Dec. 31, 2025, unless otherwise indicated. Tables on our “Metrics and data” page were updated to reflect full year 2025 data. Information regarding some known events or activities in 2026 and historical initiatives from prior years are also included. No party should place undue reliance on these forward-looking statements, which speak only as of the dates of these publications. All forward-looking statements are based on management’s knowledge and reasonable expectations at the time of publication. ExxonMobil assumes no duty to update these statements or materials as of any future date, and neither future distribution of this material nor the continued availability of this material in archive form on our website should be deemed to constitute an update or re-affirmation of these figures or statements as of any future date. Any future update will be provided only through a public disclosure indicating that fact.

See “ABOUT THE ADVANCING CLIMATE SOLUTIONS AND SUSTAINABILITY REPORTS” at the end of this document for additional information on these reports and the use of non-GAAP and other financial measures.

ABOUT THE ADVANCING CLIMATE SOLUTIONS AND SUSTAINABILITY REPORTS

The Advancing Climate Solutions Report contains terms used by the third-party disclosure frameworks. In doing so, ExxonMobil is not obligating itself to use any terms in the way defined or interpreted by any third-party, nor is it obligating itself to comply with any specific recommendation of such parties or to provide any specific disclosure. For example, with respect to the term “material,” individual companies are best suited to determine what information is material, under the long-standing U.S. Supreme Court definition, and whether to include this information in U.S. Securities and Exchange Act filings. The Sustainability Report and Advancing Climate Solutions Report are each a voluntary disclosure and are not designed to fulfill any U.S., foreign, or third-party required reporting framework.

Forward-looking and other statements regarding environmental and other sustainability efforts and aspirations are not intended to communicate any material investment information under the laws of the United States or elsewhere or represent that these are required disclosures in any other context or jurisdiction. These publications are not intended to imply that ExxonMobil has access to any significant non-public insights on future events that the reader could not independently research. In addition, historical, current, and forward-looking environmental, climate-related, and other sustainability-related statements may be based on standards for measuring progress that are still developing, internal controls and processes that continue to evolve, and assumptions that are subject to change in the future, including future laws and rulemaking. Forward-looking and other statements regarding environmental and other sustainability efforts and aspirations are for informational purposes only and are not intended as an advertisement for ExxonMobil’s equity, debt, businesses, products, or services and the reader is specifically notified that any investor-requested disclosure or future required disclosure is not and should not be construed as an inducement for the reader to purchase any product, services, or security. The statements and analysis in these publications represent a good faith effort by the Company to address these investor requests despite significant unknown variables and at times inconsistent market data, government policy signals, and calculation methodologies and reporting standards.

Actions needed to advance ExxonMobil’s 2030 greenhouse gas emission-reductions plans are incorporated into its medium-term business plans, which are updated annually. The reference case for planning beyond 2030 is based on the Company’s Global Outlook research and publication. The Global Outlook is reflective of the existing global policy environment and an assumption of increasing policy stringency and technology improvement to 2050. However, the Global Outlook does not attempt to project the degree of required future policy and technology advancement and deployment for the world, or ExxonMobil, to meet net zero by 2050. As future policies and technology advancements emerge, they will be incorporated into the GIobal Outlook, and the Company’s business plans will be updated as appropriate. References to projects or opportunities may not reflect investment decisions made by the corporation or its affiliates. Individual projects or opportunities may advance based on a number of factors, including availability of stable and supportive policy, permitting, technological advancement for cost-effective abatement, insights from the company planning process, and alignment with our partners and other stakeholders. Capital investment guidance in lower-emission and other new investments is based on our corporate plan; however, actual investment levels will be subject to the availability and attractiveness of investment opportunities, market conditions, stable public policy support, other factors, and focused on returns.

Energy demand modeling is forward-looking by nature aims to replicate integrated dynamics of the global energy system but necessarily involves simplifications to simulate its complexity. The reference to any modeled scenario or any pathway for an energy transition or expansion, including any potential net-zero scenario, does not imply ExxonMobil views any particular scenario as likely to occur. In addition, energy demand scenarios require assumptions on a variety of parameters. As such, the outcome of any given scenario using an energy demand model comes with a high degree of uncertainty. Third-party scenarios discussed in these reports reflect the modeling assumptions and outputs of their respective authors, not ExxonMobil, and their use or inclusion herein is not an endorsement by ExxonMobil of their underlying assumptions, likelihood, or probability. Investment decisions are made on the basis of ExxonMobil’s separate planning process but may be secondarily tested for robustness or resiliency against different assumptions, including against various scenarios. These reports contain information from third parties. ExxonMobil makes no representation or warranty as to the third-party information. Where necessary, ExxonMobil received permission to cite third-party sources, but the information and data remain under the control and direction of the third parties. ExxonMobil has also provided links in this report to third-party websites for ease of reference. ExxonMobil’s use of the third-party content is not an endorsement or adoption of such information.

ExxonMobil reported emissions, including reductions and avoidance performance data, are based on a combination of measured and estimated data. We assess our performance to support continuous improvement throughout the organization using our Environmental Performance Indicator (EPI) manual. The reporting guidelines and indicators in the Ipieca, the American Petroleum Institute (API), the International Association of Oil and Gas Producers Sustainability Reporting Guidance for the Oil and Gas Industry (5th edition, 2025) and key chapters of the GHG Protocol inform the EPI and the selection of the data reported. Emissions reported are estimates only, and performance data depends on variations in processes and operations, the availability of sufficient data, the quality of those data and methodology used for measurement and estimation. Emissions data is subject to change as methods, data quality, and technology improvements occur, and changes to performance data may be updated. Emissions, reductions, abatements and enabled avoidance estimates for non-ExxonMobil operated facilities are included in the equity data and similarly may be updated as changes in the performance data are reported. ExxonMobil’s plans to reduce emissions are good-faith efforts based on current relevant data and methodology, which could be changed or refined. ExxonMobil works to continuously improve its approach to estimate, detect, measure, and address emissions. ExxonMobil actively engages with industry, including API and Ipieca, to improve emission factors and methodologies, including measurements and estimates.

Any reference to ExxonMobil’s support of, work with, or collaboration with a third-party organization within these publications do not constitute or imply an endorsement by ExxonMobil of any or all of the positions or activities of such organization. ExxonMobil participates, along with other companies, institutes, universities and other organizations, in various initiatives, campaigns, projects, groups, trade organizations, and other collaborations among industry and through organizations like the United Nations that express various ambitions, aspirations and goals related to climate change, emissions, sustainability, and an energy transition or expansion. ExxonMobil’s participation or membership in such collaborations is not a promise or guarantee that ExxonMobil’s individual ambitions, future performance or policies will align with the collective ambitions of the organizations or the individual ambitions of other participants, all of which are subject to a variety of uncertainties and other factors, many of which may be beyond ExxonMobil’s control, including government regulation, availability and cost-effectiveness of technologies, and market forces, geopolitical, realignment, conflicts and other risks and uncertainties. Such third parties’ statements of collaborative or individual ambitions and goals frequently diverge from ExxonMobil’s own ambitions, plans, goals, commitments and investments. ExxonMobil will continue to make independent decisions regarding the operation of its business, including its climate-related and sustainability-related ambitions, plans, goals, commitments, and investments. ExxonMobil’s future ambitions, plans, goals commitments, and investments reflect ExxonMobil’s current plans, and ExxonMobil may unilaterally change them for various reasons, including adoption of new reporting standards or practices, market conditions; changes in its portfolio; and financial, operational, regulatory, reputational, legal and other factors.

References to “resources,” “resource base,” and similar terms refer to the total remaining estimated quantities of oil and natural gas that are expected to be ultimately recoverable. The resource base includes quantities of oil and natural gas classified as proved reserves, as well as quantities that are not yet classified as proved reserves, but that are expected to be ultimately recoverable. The term “resource base” is not intended to correspond to SEC definitions such as “probable” or “possible” reserves. For additional information, see the “Frequently Used Terms” on the Investors page of the Company’s website at www.exxonmobil.com under the header “Modeling Toolkit.” References to “oil” and “gas” include crude, natural gas liquids, bitumen, synthetic oil, and natural gas. The term “project” as used in these publications can refer to a variety of different activities and does not necessarily have the same meaning as in any government payment transparency reports.

Exxon Mobil Corporation has numerous affiliates, many with names that include ExxonMobil, Exxon, Mobil, Esso, and XTO. For convenience and simplicity, those terms and terms such as “Corporation,” “company,” “our,” “we,” and “its” are sometimes used as abbreviated references to one or more specific affiliates or affiliate groups. Abbreviated references describing global or regional operational organizations, and global or regional business lines are also sometimes used for convenience and simplicity. Nothing contained herein is intended to override the corporate separateness of affiliated companies. Exxon Mobil Corporation’s goals do not guarantee any action or future performance by its affiliates or Exxon Mobil Corporation’s responsibility for those affiliates’ actions and future performance, each affiliate of which manages its own affairs. For convenience and simplicity, words like venture, joint venture, partnership, co-venturer and partner are used to indicate business relationships involving common activities and interests, and those words may not indicate precise legal relationships. These publications cover Exxon Mobil Corporation’s owned and operated businesses and do not address the performance or operations of our suppliers, contractors or partners unless otherwise noted. In the case of certain joint ventures for which ExxonMobil is the operator, we often exercise influence but not control. Thus, the governance, processes, management and strategy of these joint ventures may differ from those in these reports. ExxonMobil completed the acquisitions of Denbury Inc. and Pioneer Natural Resources Company in 2023 and 2024, respectively. These reports and the data therein do not speak of these companies’ pre-acquisition governance, risk management, strategy approaches, or emissions or sustainability performance unless specifically referenced.

These reports or any material therein are not to be used or reproduced without the permission of Exxon Mobil Corporation. All rights reserved

SUPPLEMENTAL INFORMATION FOR NON-GAAP AND OTHER MEASURES

The Positioned for Growth in a Lower-Emission Future section of the Advancing Climate Solutions Report mentions our assessment of the strength our business and investment portfolio against a range of future outcomes, including third-party scenarios. The Company believes this can be helpful in assessing the resiliency of the business to generate cash from different potential future markets. The performance data presented in the Advancing Climate Solutions Report and Sustainability Report, including on emissions, is not financial data and is not GAAP data.